There are a great deal of methods to generate passive earnings. Among the best methods to complement portfolio progress is to hunt out dividend shares.

However in terms of dividend earnings, do you know that some alternatives could also be extra dependable than others?

Let’s break down 5 firms which can be established dividend payers, and assess why holding every of those shares over a long-term time horizon can result in large features to your portfolio.

1. Hercules Capital

Hercules Capital (NYSE: HTGC) is a enterprise growth firm (BDC). BDCs are a dependable supply of dividend earnings as a result of these firms are required to pay out at the very least 90% of their taxable earnings to traders every year.

Whereas there are various sorts of BDCs, Hercules primarily focuses on high-yield loans to start-ups within the expertise, life sciences, and renewable power industries. Though start-ups might be dangerous, Hercules has demonstrated that it employs strong due diligence processes earlier than investing. Over time, the corporate has labored with notable companies together with Unattainable Meals, Enphase Power, and Lyft.

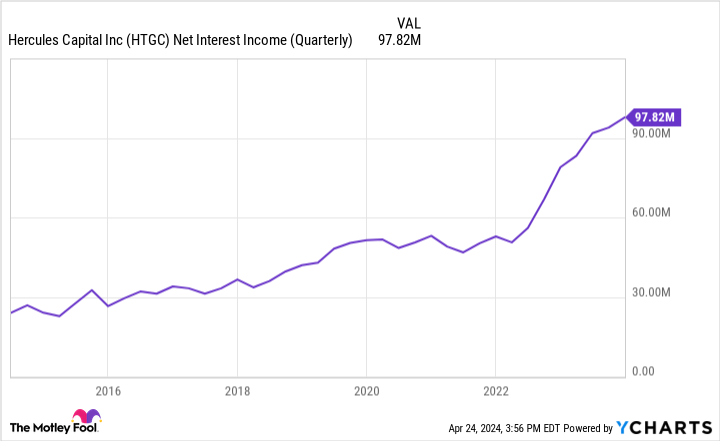

The corporate’s constant rise in web curiosity earnings undermines Hercules’ sturdy efficiency and its confirmed capacity to reward shareholders.

During the last 10 years, Hercules inventory has a complete return of 275%. Not solely does this emphasize the significance of reinvesting dividends, however it additionally highlights that Hercules has been a profitable funding over the long term.

With its juicy dividend yield of 10.4%, now might be an important alternative to scoop up shares in Hercules inventory.

2. Ares Capital

One other outstanding BDC is Ares Capital (NASDAQ: ARCC). Not like Hercules, Ares does not sometimes work with high-profile tech firms which have raised funds from enterprise capital corporations.

Somewhat, most of the firms in Ares’ portfolio are decrease center market companies that go missed by funding banks or non-public fairness traders.

Furthermore, whereas Hercules focuses on fundamental debt devices corresponding to time period loans or revolvers (assume a company line of credit score), Ares presents extra refined merchandise — together with leveraged buyouts (LBOs).

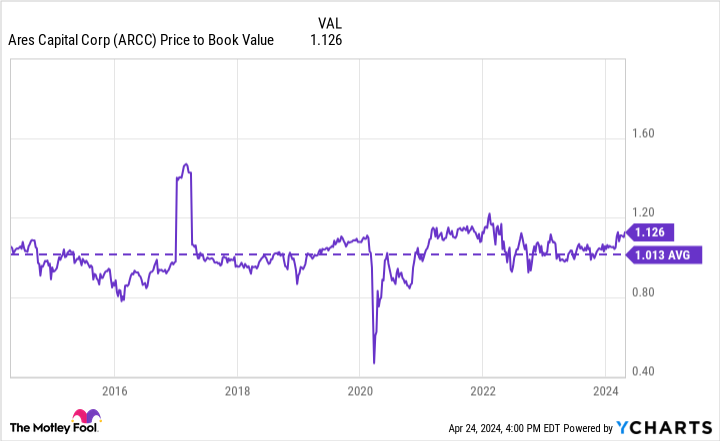

At a price-to-book (P/B) ratio of simply 1.1, Ares inventory is buying and selling basically in keeping with its 10-year common. Contemplating the corporate’s whole return has outperformed the S&P 500 during the last three- and five-year intervals, I believe now seems to be like a good time to purchase some shares in Ares at a 9.3% yield and put together to carry for the long-run.

3. Rithm Capital

Actual property funding trusts (REITs) are one other nice supply of dividend earnings.

Story continues

Rithm Capital (NYSE: RITM) is a REIT that makes a speciality of monetary companies together with mortgage origination, in addition to industrial actual property and single-family leases.

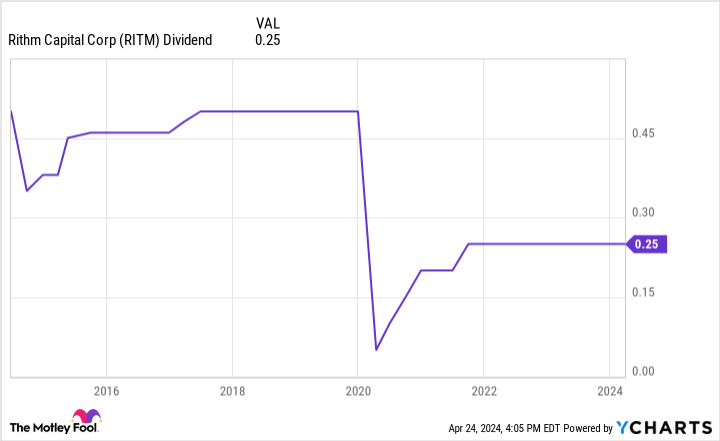

One disadvantage that traders may even see with Rithm is the corporate’s publicity to broader themes in actual property. Certainly, lingering inflation and excessive borrowing prices have affected customers, companies, and even dwelling homeowners or renters. For me, the largest mark is what Federal Reserve will resolve to do relating to rates of interest this yr.

The chart beneath illustrates how these macroeconomic variables can impression Rithm’s enterprise particularly. Whereas the dividend is decrease than it was in years previous, I believe the larger concept is that holding for the long-term might be choice.

With the inventory buying and selling at lower than $11 per share, now might be a tempting time to contemplate shopping for some shares at a 9.2% yield and the potential for a rising dividend relying on the broader macro surroundings.

4. Power Switch

Exterior of monetary companies, traders can discover profitable sources of dividend earnings from the power sector. Power Switch (NYSE: ET) is a grasp restricted partnership (MLP) working within the pure fuel trade.

MLPs have an attention-grabbing working construction as a result of these entities go earnings and losses alongside to their traders. This may be a gorgeous characteristic for earnings traders.

MLPs additionally are inclined to distribute extra income to restricted companions (LPs). These funds are often called distributions and are just like dividends.

One threat value declaring is that the power sector can expertise extra pronounced volatility than different sectors. For instance, present geopolitical situations in Europe and the Center East have drastically affected legislative coverage surrounding the power trade.

Nevertheless, Power Switch is extra insulated from these dangers. A typical theme amongst MLP’s is that these firms usually enter long-term mounted payment contracts with their prospects. In essence, this gives Power Switch with far much less publicity to commodity-based threat when in comparison with different sorts of power companies.

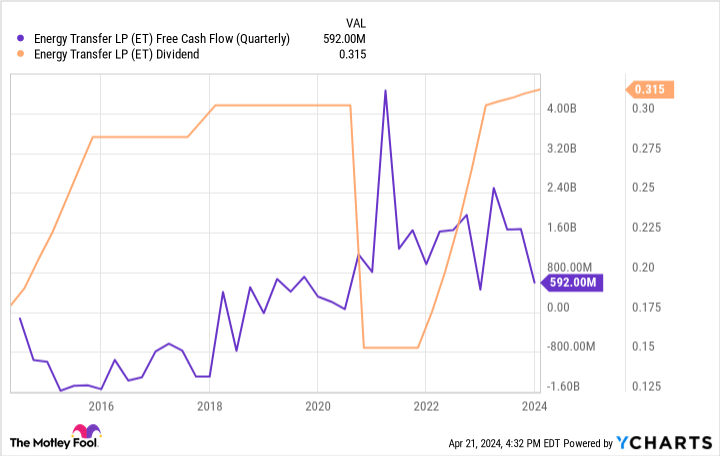

The chart beneath illustrates Power Switch’s free money move during the last 10 years. Whereas it is improved dramatically during the last decade, traits in more moderen years do present that even steadier companies corresponding to MLP’s can expertise some stage of volatility.

However, Power Switch has made it some extent to lift its distributions to traditionally excessive ranges. I believe this showcases administration’s selections to prioritize shareholders.

5. Enterprise Merchandise Companions

The final firm on my record is midstream power specialist Enterprise Merchandise Companions (NYSE: EPD).

Earlier this yr, Enterprise Merchandise Companions introduced that it was buying three way partnership pursuits from Western Midstream Companions. In early April, the corporate additionally introduced that it was breaking floor on a sequence of latest pure fuel vegetation within the Permian Basin. Amongst all of its initiatives, Enterprise Merchandise Companions has roughly $6.5 billion of authorized new enterprise at present underneath building.

What I like most about Enterprise Merchandise Companions is the corporate’s capacity to navigate difficult financial intervals whereas nonetheless rewarding shareholders. During the last 15 years, the financial system has witnessed the 2008-2009 Nice Recession, extended cratering oil costs between 2014 and 2016, and most lately the COVID-19 pandemic.

Throughout, this time, the corporate’s adjusted money move from operations (CFFO) has rise from $1.29 per unit on the finish of 2009, to $3.70 by the tip of 2023. Given the corporate’s 7.1% yield and powerful efficiency within the long-run, now might be an attention-grabbing time to contemplate shopping for some shares.

Must you make investments $1,000 in Ares Capital proper now?

Before you purchase inventory in Ares Capital, think about this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they consider are the 10 greatest shares for traders to purchase now… and Ares Capital wasn’t one in all them. The ten shares that made the reduce might produce monster returns within the coming years.

Take into account when Nvidia made this record on April 15, 2005… in the event you invested $1,000 on the time of our suggestion, you’d have $537,557!*

Inventory Advisor gives traders with an easy-to-follow blueprint for achievement, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of April 22, 2024

Adam Spatacco has no place in any of the shares talked about. The Motley Idiot has positions in and recommends Enphase Power. The Motley Idiot recommends Enterprise Merchandise Companions. The Motley Idiot has a disclosure coverage.

Trying For Passive Earnings? Right here Are 5 Extremely-Excessive-Yield Dividend Shares to Purchase and Maintain For a Decade was initially printed by The Motley Idiot