Sundown sky with Duke Power constructing in Charlotte, NC Takako Hatayama-Phillips

Duke Power Company (NYSE:DUK) has each power utilities and infrastructure enterprise in addition to the gasoline utilities & infrastructure enterprise. Primarily regulated, this duo types the 2 major reporting segments for this firm, with the stability of actions falling below the all encompassing “different”.

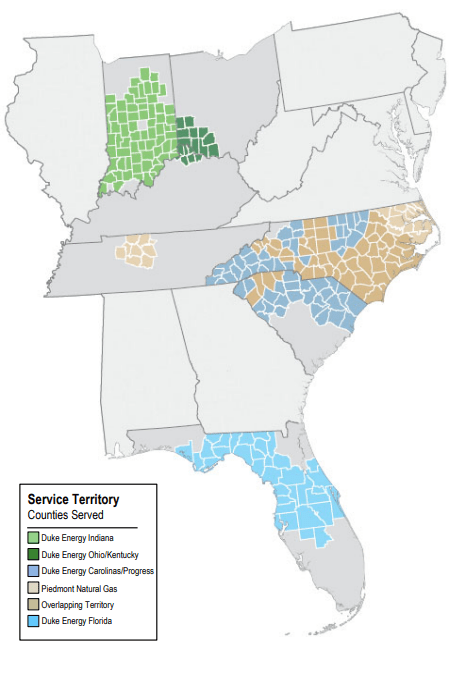

Its power utilities & infrastructure operations comprise technology, transmission, distribution, and sale of electrical energy. This arm serves over 8 million retail clients within the Carolinas, Florida, Indiana, Ohio and Kentucky. Duke additionally serves the wholesale electrical energy wants of consumers like municipalities and cooperative utilities below this setup. The enterprise generates electrical energy utilizing primarily pure gasoline and gas oil, nuclear power, and coal. Duke’s gasoline utilities & infrastructure operation companies round 1.7 million clients and consists of residential, industrial, industrial, and energy technology pure gasoline clients, together with municipalities. Geographically, the purchasers for this operation are situated within the Carolinas, Tennessee, Ohio and Northern Kentucky.

Q1-2024 Presentation

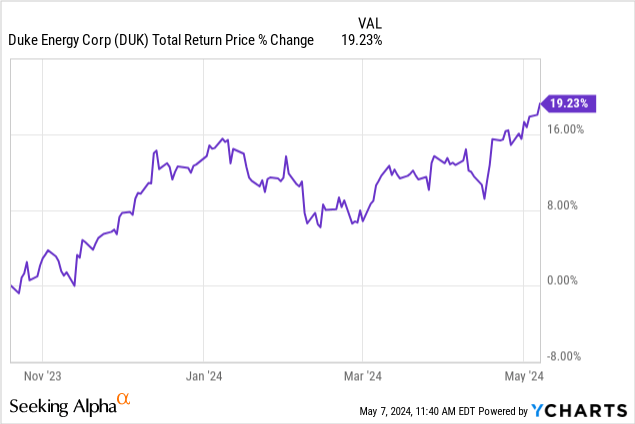

We have now lined this Fortune 150 firm final October, and we gave it a “maintain” score or in different phrases, we stayed on the sidelines. It has made a whopping 19% and alter for its traders since then.

We believed that this utility firm was able to making 7-8% yearly from that time (and mentioned as a lot in that piece), however risk-free or high quality bonds would get us that anyway. We outlined the danger components of proudly owning a utility when rates of interest have been excessive.

Gone are the times of zero % and utilities are susceptible as they roll over their huge debt hundreds. One different issue right here is the recognition of closed finish funds which have dialed up the leverage on utilities. To take care of the identical stage of leverage in a down market, they need to promote the underlying securities and this might proceed to maintain these shares pressured.

Supply: Duke Power: Strong Utility With A Good Development Profile

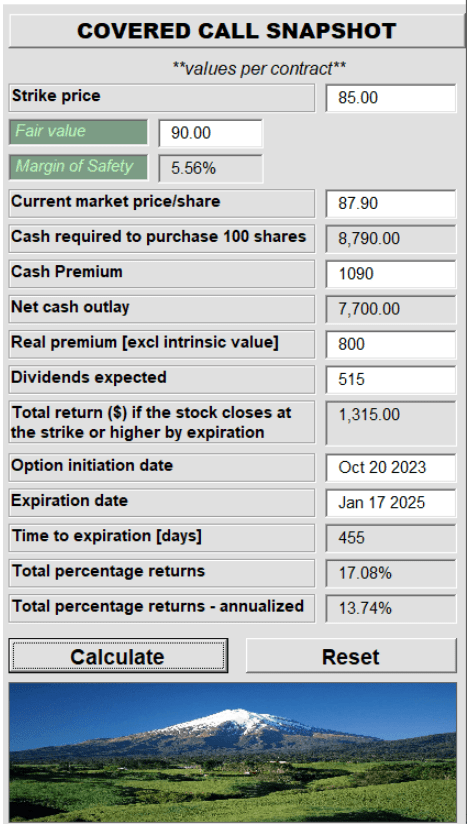

We steered an in-the-money lined name play to lock in near 14%, as a substitute for traders that wished a bit of the motion.

Looking for Alpha Article

We sometimes select the trail of least volatility for our investments and like to get our annualized return repair through choices. The commons outperformed the choice play on this case, however in hindsight, we might nonetheless select the draw back safety through calls below the present macro circumstances.

Duke’s Q1 outcomes are recent off the oven, and we’ll take the chance to evaluation the numbers and replace our thesis.

Q1-2024 Outcomes & Outlook

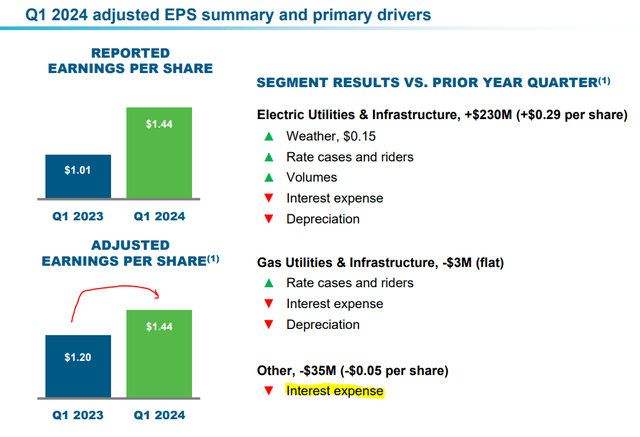

Duke delivered a powerful Q1-2024, with adjusted earnings vaulting from $1.20 to $1.44 per share. The first driver was climate, which added 15 cents, and the remaining got here from fee instances and ROEs on increasing value. Curiosity expense was a small detractor, however the Duke’s effectively spaced out maturities have minimized financing wants throughout rising charges.

Q1-2024 Presentation

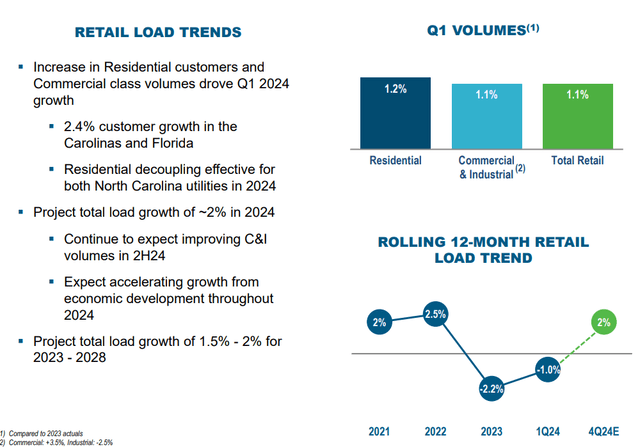

The important thing purpose for proudly owning regulated utilities is that you’re making a play on volumes. Duke’s volumes in Q1-2024 have been tepid, however the utility expects a rising development within the later quarters of the yr.

Q1-2024 Presentation

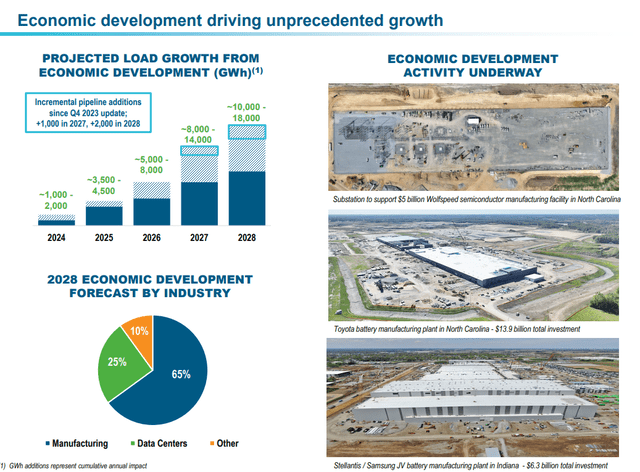

There’s some widespread growth from the onshoring development in play, and quantity development from each information facilities and manufacturing may push Duke handed the two% ranges in late 2024 and 2025.

Q1-2024 Presentation

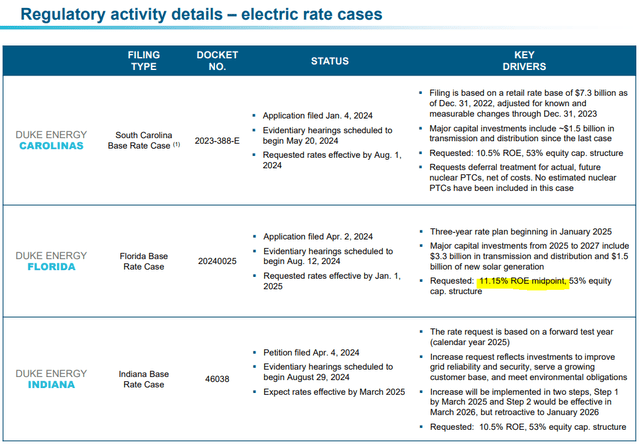

On the regulatory entrance, the corporate continues to have a number of the most favorable settings you’ll find. One instance right here is highlighted, the place Duke is requesting 11.15% ROE.

Q1-2024 Presentation

Clearly, them requesting it doesn’t imply they’ll get it. However utilities know the way the sport is performed, they usually are likely to ask across the ballpark of what they count on. You’ll be able to distinction that quantity with what different utilities across the nation are getting.

Administration affirmed that they have been nonetheless headed for $5.85 to $6.10 in adjusted earnings for the yr, and the inventory has been doing extraordinarily effectively of late.

Valuation

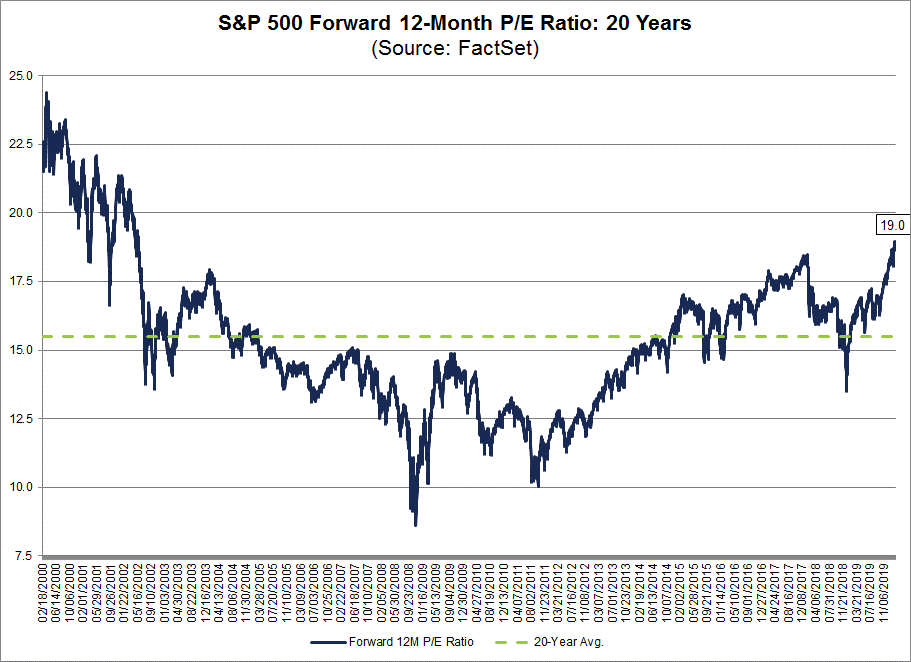

At 17X earnings, Duke might not seem extraordinarily costly for a utility delivering 6% development.

Looking for Alpha

That has been the mantra from administration that you simply add the 4% yield to six% development, and also you get 10% with very low threat. This in flip, in fact, pushes the fill up and makes fairness issuance very candy. So you’ve a self-fulfilling prophecy of types. There’s usually not a lot we are able to discover fallacious with the concept besides that these 17X-20X multiples have turn into regular, solely from a Zero Curiosity Price Coverage (ZIRP) perspective. For those who study the non-ZIRP period of 2004-2008 (even earlier than the crash), most utilities traded effectively beneath that vary.

FactSet

This stays the hazard right here and one which can lead to a major blowback. Most traders are likely to say that they will ignore that so long as the dividends ring into the financial institution on time. However with persistent debt and fairness issuers like REITs and utilities, the price of fairness will not be one thing to be taken calmly. If the inventory drops sufficient, all of your earnings estimates will drop as effectively. This may even have a blowback on credit score rankings. So Duke right here is at finest a “maintain/impartial” and is quickly converging at some extent the place we would even be capable of go to a “Promote”.

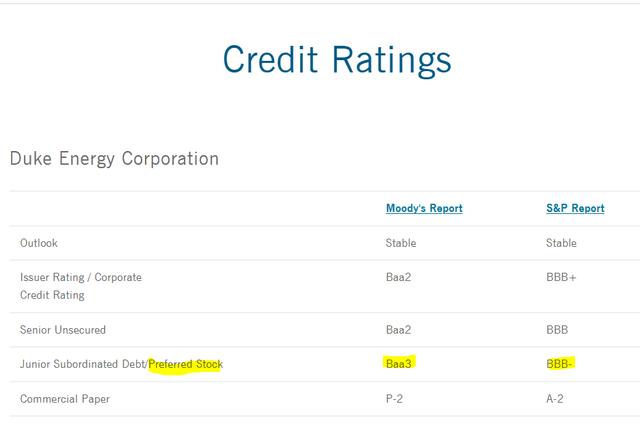

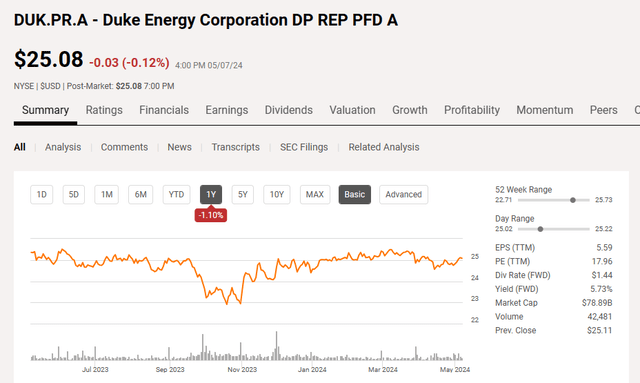

Duke Power Company DP REP PFD A (NYSE:DUK.PR.A)

These wanting a daily revenue stream from a high quality utility have typically gone up the capital inventory. Duke is certainly one to have a most well-liked share that also makes the final rung of the funding grade ladder.

Q1-2024 Duke Power

At current, the inventory is buying and selling close to par and presents a 5.8% stripped (subsequent ex-dividend date is Might 15, 2024) yield.

Looking for Alpha

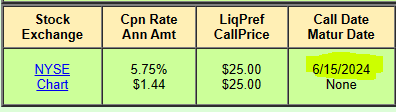

This isn’t notably dangerous, however not one we are able to get actually enthusiastic about both. Even should you imagine rates of interest are about to go to zero within the subsequent 2 years, it’s a must to remember that this may be redeemed at $25.00 at any level after June 15, 2024.

Quantum On-line

There are much better prospects right here in right this moment’s market, and we might give this a cross as effectively.

{kind=link}