jroballo

Introduction

On February 20, 2022, I wrote an article titled Albemarle: One Of My Favourite Trades Going Ahead. It was the primary article I wrote on the Albemarle Company (NYSE:ALB).

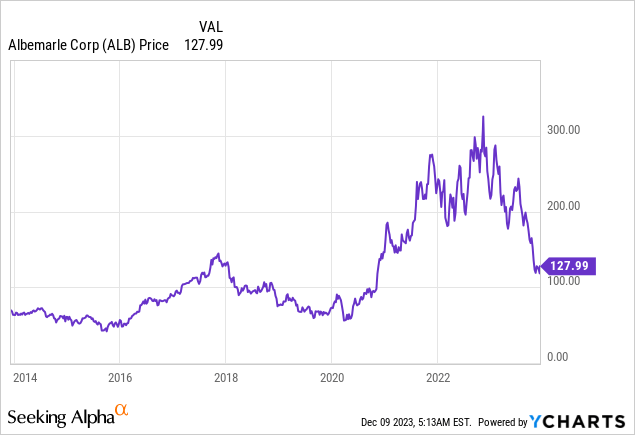

After publication, the inventory rose by greater than 80%.

Sadly, the inventory is now down 60% from its peak, falling 40% year-to-date. It is now the ninth worst performer of the S&P 500.

Whereas this can be unhealthy for traders who had been late to the get together, I consider that Albemarle gives great worth at present costs.

Not solely is ALB a dividend aristocrat with a historical past of greater than 25 consecutive annual dividend hikes, however evidently business headwinds from falling lithium costs are beginning to ease, offering (potential) ALB traders with a horny danger/reward.

So, with all of this in thoughts, let’s take a more in-depth look on the firm!

What’s Up With ALB?

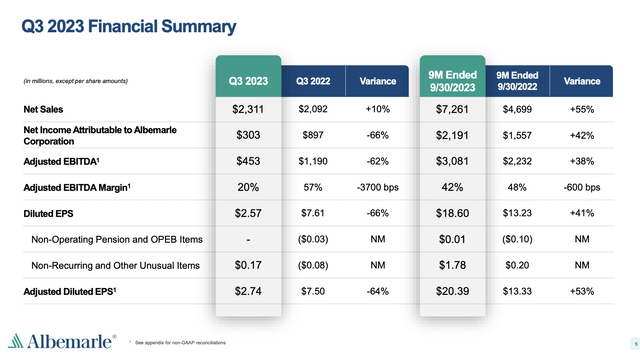

Lithium is not in an incredible spot, which is mirrored in Albemarle’s most up-to-date monetary outcomes.

For instance, the third-quarter adjusted EBITDA was $453 million, down 62% year-over-year, primarily as a consequence of softer lithium market pricing and timing impacts.

Albemarle Company

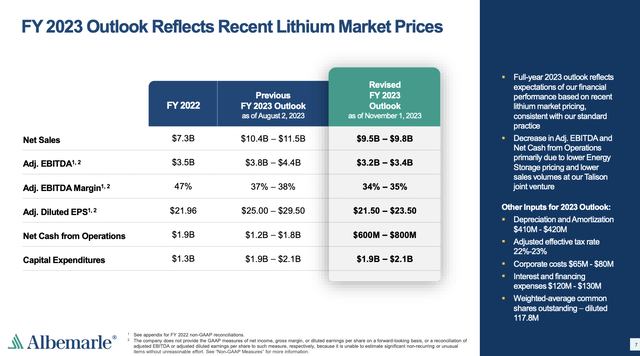

In consequence, the corporate lowered its whole outlook for 2023, with a spread of $9.5 billion to $9.8 billion in internet gross sales, and adjusted EBITDA anticipated to be within the vary of $3.2 billion to $3.4 billion.

Adjusted EPS outlook was adjusted to $21.50 to $23.50.

Albemarle Company

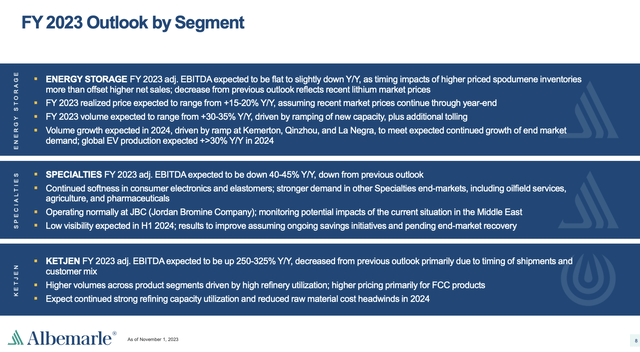

Particularly, the power storage section, which accounted for greater than 60% of 2022 internet gross sales, is predicted to have internet gross sales within the vary of $7 billion to $7.2 billion in 2023, with adjusted EBITDA flat to barely down.

Specialties section internet gross sales are projected to be roughly $1.5 billion, with adjusted EBITDA down 40% to 45% year-over-year.

Ketjen’s 2023 full-year adjusted EBITDA is predicted to be up 250% to 325% year-over-year.

Albemarle Company

On prime of that, the corporate stopped its pursuit to purchase Liontown in October.

Albemarle CEO Kent Masters mentioned in a press release that transferring ahead with the Liontown acquisition was not in his firm’s finest pursuits and was in step with its disciplined method to capital allocation. – Reuters

Reuters

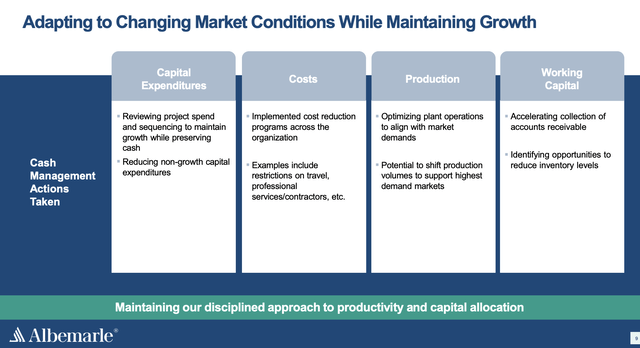

As an alternative of being an aggressive purchaser, the corporate is proactively addressing value administration via a complete evaluation of actions aimed toward supporting near-term profitability and money movement.

The corporate is strategically managing its undertaking spend and sequencing to protect money. This features a discount in noncritical journey and discretionary spending, demonstrating a dedication to disciplined monetary practices – particularly on this market setting.

Albemarle Company

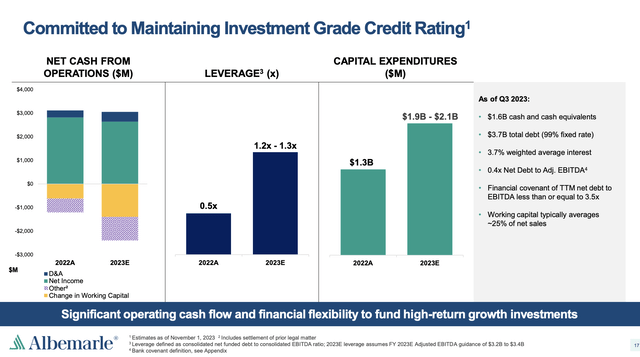

In manufacturing, Albemarle is exceeding its objective of $170 million in productiveness advantages for 2023.

This contains enhancements in total gear effectiveness to boost yield and utilization, anticipated to yield over $70 million in advantages.

The corporate is strategically sourcing uncooked supplies to seize decrease pricing, contributing to elevated effectivity and cost-effectiveness.

Trying ahead to 2024, Albemarle plans to construct on these initiatives, focusing on extra advantages throughout manufacturing, procurement, and back-office operations.

This additionally contains sustaining a wholesome stability sheet. Regardless of the decline in EBITDA, the corporate expects to maintain its internet leverage ratio beneath 1.4x (EBITDA) this yr. Virtually all of its debt has a hard and fast fee. The weighted common rate of interest on its debt is simply 3.7%.

Albemarle Company

The corporate has an investment-grade credit standing of BBB.

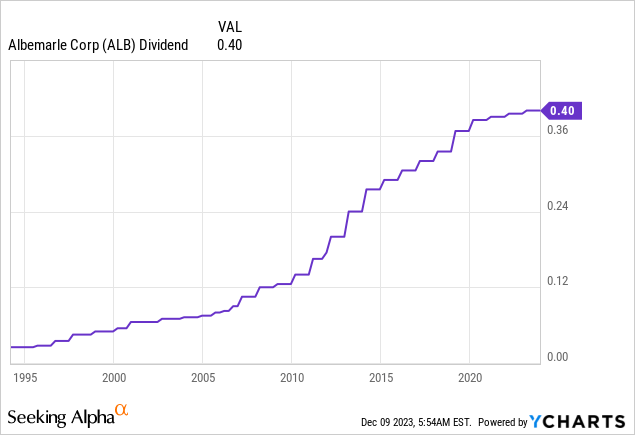

It additionally has a dividend that has been hiked for 28 consecutive years, though I can’t make the case that ALB must be purchased for its dividend.

The corporate yields simply 1.3%, and regardless of having a payout ratio of lower than 6%, its five-year dividend CAGR is 3.8%.

What makes ALB engaging is its valuation and the alternatives within the lithium business.

Mild At The Finish Of The Tunnel

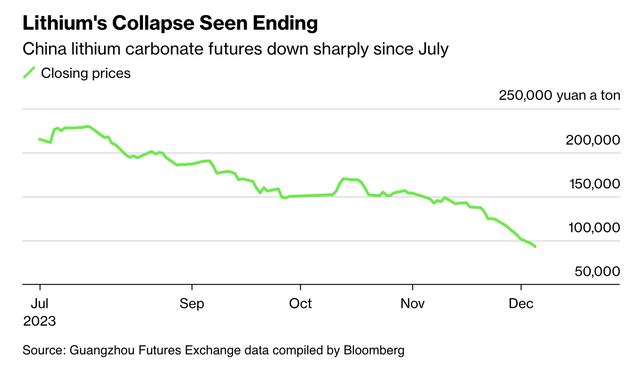

On December 6, Bloomberg wrote an article on ongoing developments within the lithium business.

Reuters

In response to the article, the lithium carbonate futures for January supply on the Guangzhou Futures Change trades at roughly 92,450 yuan ($12,915) a ton, down from its peak of over 200,000 yuan in July.

Now, analysts recommend that the downward pattern for lithium is nearing its finish, projecting a bottom-out between 80,000 and 90,000 yuan a ton.

Bloomberg

Sadly, it is a powerful name to make.

Regardless of expectations of stabilization, challenges persist within the lithium market.

A surge in provide and a slowdown in electrical car gross sales progress have contributed to the present downturn.

The worldwide market just isn’t anticipated to return to a deficit till 2028, in accordance with Bloomberg, which used Benchmark Mineral Intelligence knowledge.

Trying forward, the query arises whether or not the present cycle of decrease lithium costs will lead corporations to cancel or delay plans for brand new mines or refineries.

Additionally, the necessity for coverage assist from governments aiming to construct their very own provide chains turns into essential. Albemarle has already noticed cancellations and delays in response to market circumstances.

I consider that huge financial challenges in China and the general strain on (typically very costly) electrical car gross sales in an setting of subdued client confidence are placing the brakes on a bull case that used to thrive on numerous confidence and sky-high expectations.

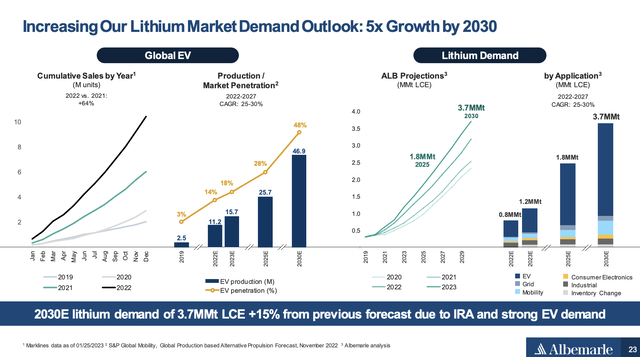

Nevertheless, I do agree with Albemarle that the long-term bull case stays sturdy. Whereas I am not a fan of the EV pattern (I want the gradual adoption of latest applied sciences, beginning with a push for hybrid autos), it seems just like the EV market penetration will proceed to rise, probably reaching 50% in 2030.

This might push lithium demand to three.7 million metric tons per yr, as we will see within the chart beneath. Word that Albemarle has constantly hiked its long-term outlook.

Albemarle Company

Albemarle is predicted to develop its lithium volumes by no less than 20% per yr throughout this era, breaching the 300-kiloton mark by 2027.

It additionally helps that the corporate is now buying and selling at a deep low cost.

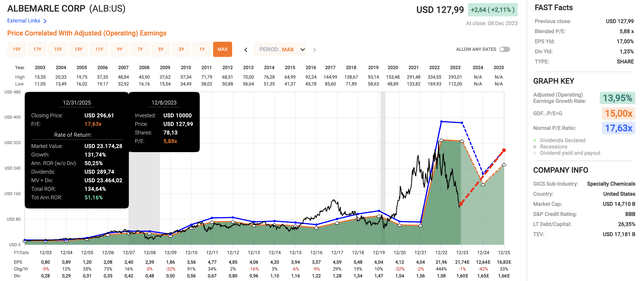

Utilizing the info within the chart beneath:

This yr, ALB is predicted to see a 1% EPS contraction, adopted by a 42% decline in 2024. 2025 is predicted to see a 33% restoration, which I anticipate to final. At present, ALB trades at a blended P/E ratio of 5.9x. Even through the Nice Monetary Disaster, ALB was dearer! In 2008, it traded at a blended P/E ratio of 8x. The long-term normalized P/E ratio is 17.6x. A return to this valuation by incorporation of anticipated EPS progress charges would pave the way in which for a good worth near $300, which is roughly the place it was buying and selling final yr earlier than promoting off.

FAST Graphs

Whereas the attractiveness of its blended P/E ratio relies on its earnings outlook, I consider that numerous weak point has been priced in.

At this level, it seems like cyclical dangers have been massively decreased from the lithium commerce, which leaves numerous long-term secular tailwinds.

I additionally consider that the theoretical truthful worth of $300 for ALB is smart. Nevertheless, it will not go there except we see significant financial enhancements.

Therefore, regardless of my Sturdy Purchase ranking, I urge potential traders to watch out when coping with cyclical mining corporations.

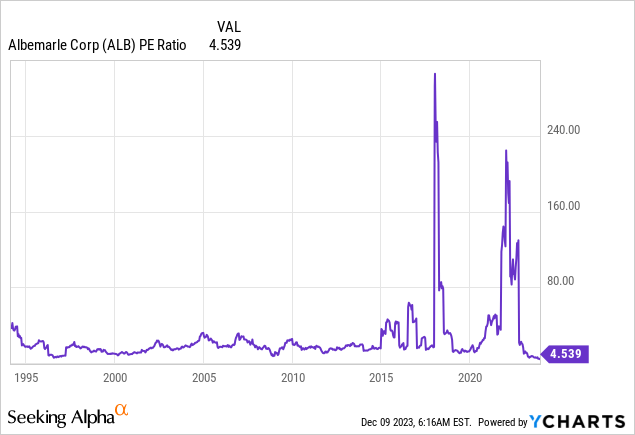

On a facet be aware, the chart beneath reveals the LTM P/E ratio going again to 1994. Though it doesn’t incorporate forward-looking earnings, it does present how important the valuation decline has been.

This brings me to the takeaway.

Takeaway

Regardless of latest challenges, Albemarle presents a compelling funding alternative.

The lithium business faces headwinds, impacting ALB’s financials.

Nevertheless, the corporate’s proactive value administration, strategic initiatives, and powerful stability sheet reveal resilience.

With a concentrate on effectivity, ALB goals to navigate the present market setting efficiently.

In the meantime, the decline in lithium costs could also be nearing its finish, with projections indicating stabilization.

ALB’s long-term outlook stays sturdy, aligning with the anticipated progress within the electrical car market.

Buying and selling at a deep low cost, ALB’s potential truthful worth of $300 suggests a big upside.

Nonetheless, regardless of being a compelling long-term prospect, traders ought to be cautious with cyclical mining corporations like ALB as a consequence of their unstable nature.

{kind=link}